In the first quarter of 2025, inflation eased in several regions but remained above target levels overall.

In the face of a more confrontational stance from the new US administration, European markets performed well, while the S&P 500 struggled, posting losses for the quarter.

Read on for a deeper look at market performance in Q1 of 2025.

UK

According to the Office for National Statistics (ONS), real GDP in the UK grew by an estimated 0.2% in the three months to January 2025, driven primarily by growth in the services sector. However, on a monthly basis, latest estimates show that GDP declined by 0.1% in January 2025.

Further data from the ONS shows that UK inflation rose by 2.8% in the 12 months to February 2025, down from 3% in January. The biggest reduction in inflationary pressure came from falling clothing prices.

Although inflation is falling, it still remains above the 2% target. In response to this, the Bank of England (BoE) lowered the base rate to 4.5% in February but maintained it in March to help encourage a further fall in inflation.

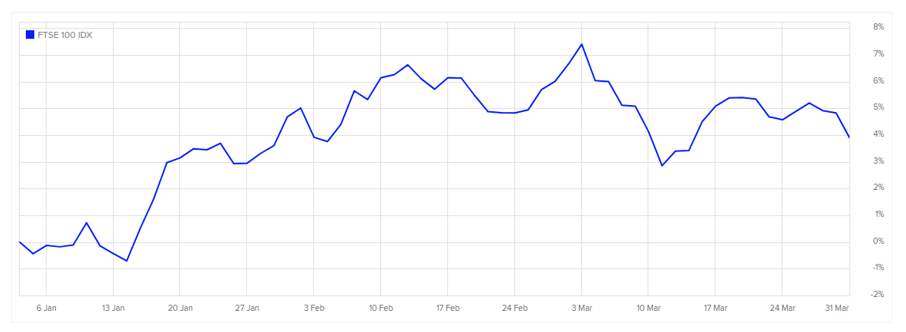

The FTSE 100 performed well in Q1, growing by around 4% – as you can see in the graph below

Source: London Stock Exchange

Furthermore, data from JP Morgan’s quarterly review shows the UK FTSE All-Share grew by 4.5% and was the second-strongest performer in Q1.

Europe

According to Eurostat, GDP grew by 0.2% in the euro area and 0.4% in the EU during the fourth quarter of 2024.

Further Eurostat data shows that annual inflation in the euro area eased to 2.2% in March 2025, down from 2.3% in February.

In response to declining inflation, the European Central Bank (ECB) cut its three key interest rates by 25 basis points.

Meanwhile, the JP Morgan review shows that the MSCI Europe ex-UK rose by 6.4%, making it the strongest performer in Q1. This is partly driven by increased defence spending, as the new US administration has signalled it is unlikely to provide the same level of support as in previous years.

US

Data from Trading Economics shows the annual inflation rate in the US eased to 2.8% in February, down from 3% in January, largely due to a 0.2% year-on-year decline in energy costs.

With inflation still above target, the Federal Reserve kept the federal funds rate unchanged at 4.25% – 4.5% during its March 2025 meeting, extending the pause in its rate-cut cycle that began in January.

Further quarterly data from Trading Economics shows that the US economy grew at a rate of 2.4% in Q4 2024, slowing from 3.1% in Q3 and 3% in Q2.

Meanwhile, the JP Morgan market review reveals that the S&P 500 was the weakest global performer in Q1, declining by 4.3%. This is partly due to ongoing uncertainty surrounding US trade policy.

Asia

JP Morgan data shows that Japan’s TOPIX declined by 3.4% in Q1, making it the second-worst performer after the US, while the MSCI Asia ex-Japan rose by 1.9%.

Meanwhile, Trading Economics reports that Japan’s annual inflation rate fell to 3.7% in February 2025, down from a two-year high of 4.0% in January.

Further data reveals that, in China, inflation dropped by 0.7% in February, reversing a 0.5% rise the previous month. This marked the first instance of deflation since January 2024, driven by fading seasonal demand after the Spring Festival in late January.

Get in touch

If you need advice on any aspect of our Q1 2025 investment update, please get in touch. To find out what we can do for you, email admin@stonegatewealth.co.uk or call us on 01785 876222.

Production

Production